Imagine dedicating your core academic career to engineering complex satellite subsystems, only to discover that entry-level positions at localized innovation hubs offer lower real-terms compensation than standard hospitality roles. Across the UK space sector, engineering graduates are entering a market where starting salaries have fundamentally decoupled from inflation, falling roughly 30 percent in real terms compared to what their predecessors commanded twenty-five years ago. This economic disparity presents a critical bottleneck for sovereign industrial ambitions.

A recent analysis published in The Register by Lindsay Clark highlighted the structural talent hurdles facing the British space sector. Drawing on insights from aerospace engineering faculty, the report identified an immediate opportunity: projected budget cuts within international space programs could trigger an influx of highly skilled engineering talent looking to relocate. The UK remains well-positioned to capture this migrating expertise—but only if its domestic corporate ecosystem can offer economically viable compensation frameworks.

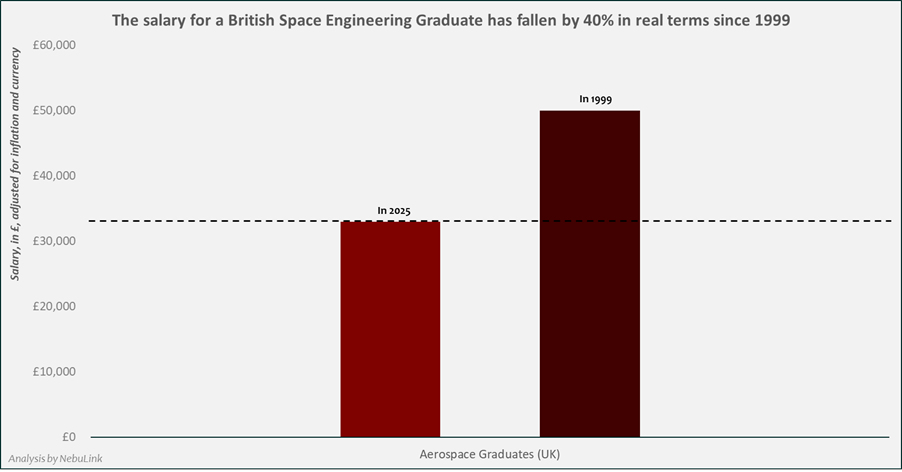

The 1999 Baseline: A Legacy of Real-Terms Stagnation

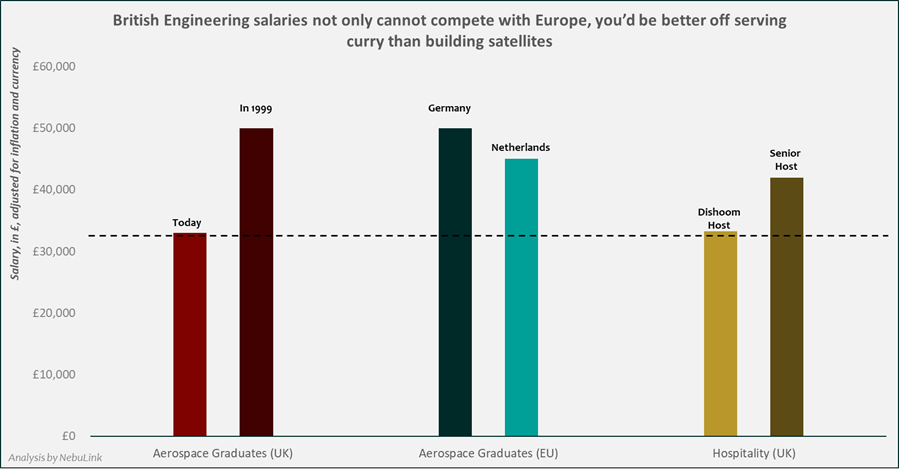

Historical market evaluations reveal a systemic devaluation of technical personnel over the past quarter-century. In the late 1990s, an entry-level graduate position within the British aerospace sector routinely paid a base salary of £20,000 per annum. When adjusted for cumulative inflation, that historical baseline equates to an estimated purchasing power of £45,000 to £50,000 today.

By contrast, contemporary aerospace engineering graduates in the UK are routinely presented with initial offers ranging between £25,000 and £35,000, with only a marginal fraction of elite technical tracks breaching the £40,000 threshold.

This trajectory represents more than simple nominal friction; it points to an institutional strategy of structural underinvestment. While macro-economic pressures and minimum wage adjustments have forced nominal starting benchmarks slightly above £30,000, the baseline strategy remains one of cost-minimization. If orbital infrastructure and satellite applications are genuinely categorized as critical national priorities, the underlying compensation frameworks must reflect that strategic classification.

The Harwell Bottleneck: Innovation Hubs with Disproportionate Costs

The financial strain of suppressed starting compensation is exacerbated by the geographic concentration of the industry. Harwell, widely championed as the centerpiece of the UK’s space innovation ecosystem, hosts a dense cluster of prominent organizations including the UK Space Agency, Open Cosmos, the Satellite Applications Catapult, and dozens of early-stage startups. On paper, this layout creates a high-value, walkable concentration of specialized expertise. In practice, it operates as an isolated, car-dependent science park embedded within the high-rent corridors of Oxfordshire.

The underlying micro-economics demonstrate why this layout struggles to retain early-career engineers:

- Average Local Rental Costs: A single room within a localized shared property near the Harwell campus averages roughly £834 per month.

- Net Graduate Take-Home Income: An engineer earning a standard entry salary of £30,000 takes home approximately £1,970 per month post-tax.

- Rental Income Allocation: Base housing costs immediately consume over 42 percent of net monthly income, before accounting for municipal taxes, utility bills, basic groceries, or localized commuting expenses.

This is not an outlier case; it is the baseline operational dynamic. A significant portion of the UK’s strategic space engineering positions are located within premium regional economies where entry-level remuneration fails to cover independent or even standard shared housing infrastructure comfortably.

The Selective Elite Track and Alternative Fields

The space sector’s primary competitor for specialized STEM talent extends beyond adjacent engineering fields; it includes any knowledge-work sector offering superior compensation with fewer technical barriers to entry. Financial and strategic management consultancies routinely capture premium analytical talent by offering starting baselines that dwarf standard engineering tracks.

While elite financial tiers—such as bulge-bracket investment banking analysts (£60,000 base) or high-frequency trading firms (£150,000 base)—are heavily gate-kept by institutional prestige, first-year internships, and specific geographic networks, they highlight a massive wage premium. The central challenge for the UK space market is not that it lags behind the absolute highest tiers of global finance, but that its base compensation model struggles to compete with accessible, domestic alternatives that carry fewer regulatory and security clearance burdens.

The Continental Premium: Evaluating European Alternatives

Talent naturally migrates to markets where technical expertise is highly valued, and continental European space hubs are increasingly out-pacing the UK’s domestic offers. Prior to recent geopolitical and visa restructurings, the UK stood as a premier destination for pan-European space professionals due to its global connectivity and competitive localized salaries. That financial premium has largely dissipated, as engineers across European space hubs see diminishing economic incentives to relocate to the UK market.

An evaluation of regional space sector compensation frameworks highlights this disparity:

- Germany: Operating under structured IG Metall collective bargaining agreements, entry-level engineering roles regularly command base salaries between €50,000 and €65,000 (£42,000 to £55,000). These frameworks are augmented by legally mandated cost-of-living adjustments, structured progression steps, and comprehensive social safety provisions.

- The Netherlands & Sweden: Early-career positions at ESA-affiliated centers like ESTEC in Noordwijk offer starting packages ranging from €45,000 to €60,000 (£38,000 to £50,000), frequently accompanied by localized housing allowances and subsidized transport infrastructure.

- Italy: Graduate engineers at primary industrial primes report starting packages between €33,000 and €35,000 (£28,000 to £30,000). While nominally closer to UK scales, these roles feature reliable incremental increases by years two and three, combined with significantly lower cost-of-living metrics outside major metropolitan hubs.

Domestic Disconnect: Technical Roles vs. Non-Graduate Sectors

While continental markets consistently outbid the UK space sector, the domestic disconnect becomes even more pronounced when contrasting high-performance engineering roles against progressive consumer services industries.

A comparative analysis of contemporary UK salary data points illustrates the narrow economic delta between these career paths:

| Professional Sector & Role | Average Annual Compensation Range |

|---|---|

| Graduate Space Engineer | £28,000 – £34,000 |

| Specialist Aerospace Position | £35,000 – £40,000 |

| Senior Systems Engineer (5+ Years Experience) | £35,000 – £45,000 |

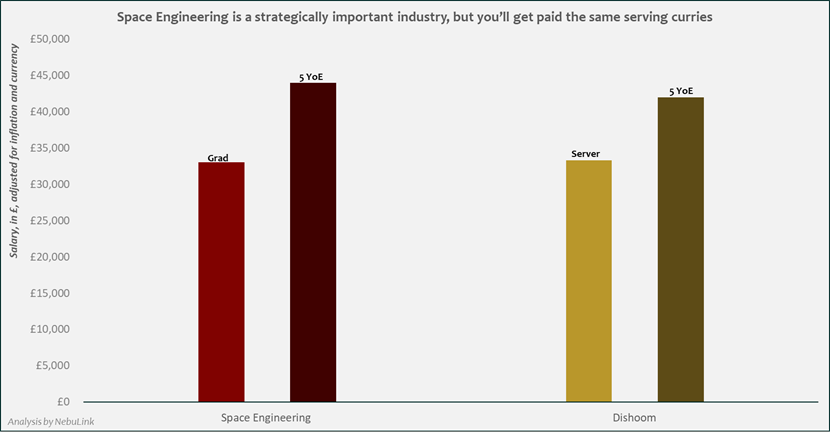

| Dishoom Hospitality Server (Base + Tronc/Tips) | £33,280 – £41,000 |

| Dishoom Hospitality Team Management | Up to £45,000 |

A professional server within a well-structured hospitality group can equal or exceed the net take-home earnings of an engineer responsible for spaceflight subsystems. Crucially, the hospitality path avoids the long-term financial drag of specialized graduate student loan repayments and intensive multi-stage technical screening processes. This comparison is not a critique of hospitality compensation models—which reflect progressive, market-rate adjustments—but rather a stark indictment of the structural wage compression within British engineering.

Conclusion: Realignment as an Operational Necessity

Sovereign orbital capabilities cannot be sustained solely on institutional goodwill and undercompensated professional labor. While national strategy white papers frequently champion STEM educational pipelines and point to grand upstream objectives, long-term operational success depends entirely on personnel retention.

Until public funding bodies and commercial aerospace primes systematically restructure entry-level packages to mitigate localized cost-of-living bottlenecks, the UK space industry will continue to experience a steady drain of its premier analytical minds. True orbital capability requires a baseline investment structure that treats engineers as essential national assets rather than disposable line-item expenditures.

NebuLink is a space market intelligence firm providing actionable data, competitive positioning matrixes, and strategic downstream market assessments. For detailed industrial reporting or tailored corporate advisory services, contact: Alistair@NebuLink.co.uk