When most people think about space, the same images come to mind: astronauts aboard the International Space Station, or the latest dramatic launch of a new rocket. These are spectacular moments that capture the imagination, but they are not where most of the real economic or societal value of space lies. Satellites orbiting above us already underpin the systems we rely on every day, whether we realise it or not. One of the least appreciated but most important areas where this impact is felt is in energy.

Working in the space sector, I often find myself having to explain to friends, family, and even taxi drivers why space matters. The conversation usually goes through the same predictable beats: no, I do not work for NASA, and no, I am not employed by SpaceX. When pressed further, I tend to rely on obvious examples of public good. It is easy enough to explain that satellites carry advanced cameras that can detect forest fires as they start, or monitor droughts from orbit, or measure crop moisture to help farmers increase yields. These examples are tangible, and they resonate with the average person.

Yet focusing too heavily on them risks missing out on other domains that are just as critical, and perhaps even more so in the years ahead. Among these overlooked areas, energy may well be the one where space makes the biggest difference in the coming decade. This article exists to explain a few novel applications in the energy field to make your taxi rides a little bit more varied.

What do we mean by energy

When we talk about energy, we are not speaking in abstract terms about a far-off policy goal. Energy is the lifeblood of the modern economy and one of Europe’s greatest vulnerabilities. The Russian invasion of Ukraine made this clear. Europe’s dependence on Russian gas left governments scrambling to secure new supplies, prop up prices for consumers, and prevent entire industries from collapsing. At the same time, China’s dominance in solar manufacturing and critical minerals has reshaped global dependencies, creating new risks and limiting Europe’s room for manoeuvre. Energy has become as much a matter of geopolitics and national security as of engineering.

The scale is staggering. The European Union spends hundreds of billions of euros each year on energy imports. Meanwhile, policymakers are attempting to decarbonise grids, integrate massive amounts of renewable energy, electrify transport, and build hydrogen infrastructure. Every stage of this system carries enormous cost and complexity.

One way to break it down is into four broad phases of the energy lifecycle: generation, storage and distribution, operations and maintenance, and decommissioning and recycling.

- Generation covers the production of power through renewables, fossil fuels, or nuclear.

- Storage and Distribution involves pipelines, grids, and increasingly hydrogen networks.

- Operations and Maintenance means the day-to-day work of keeping the lights on, ensuring reliability, and cutting costs.

- Decommissioning and Recycling concerns the safe retirement of ageing assets and the reduction of environmental impact from old infrastructure.

Each of these stages is vast, politically sensitive, and economically critical. Importantly, each also offers opportunities where space data can reduce costs, increase resilience, or improve environmental performance. That is what makes energy such a compelling case for space applications: it is not about speculative benefits in the distant future, but about tangible benefits that would bring down your energy bills.

What Is Space for Energy?

Sure, energy is important. But, what does it have to do with space? The answer is not science fiction. Satellites already provide tools that deliver value to energy companies today, across the full lifecycle of energy.

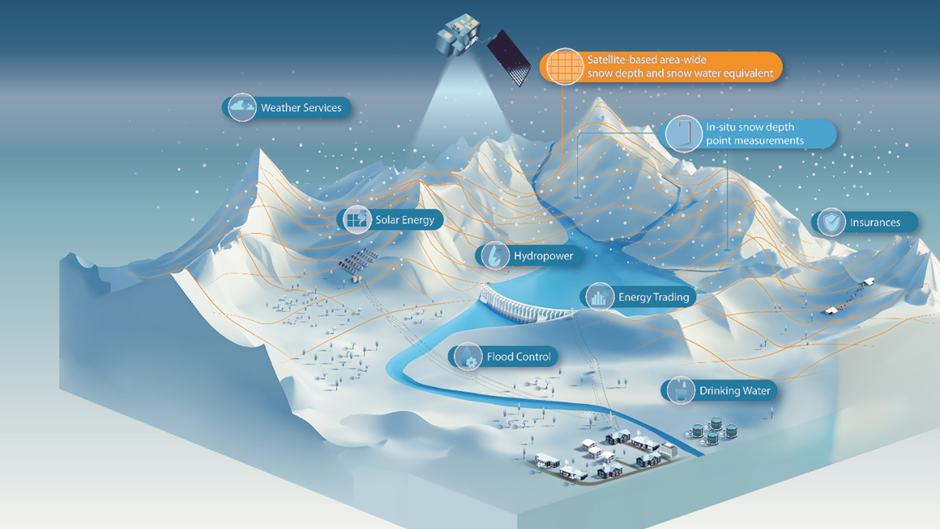

Generation: Hydropower Forecasting via Satellite

Firstly, hydropower remains the backbone of Europe’s renewable energy mix, with more than 100 gigawatts of installed capacity spread across Europe. Yet, hydro is uniquely vulnerable to something as simple as seasonal swings in rain and snowfall. We’re dealing with this today in the UK, with record low reservoirs in a dry summer. Operators, without careful forecasting, either have too much water in the reservoirs which wastes water and money, or they leave them too empty during summer, forcing them to buy electricity at a higher cost. Either way, that’s tens of millions of pounds wasted per reservoir.

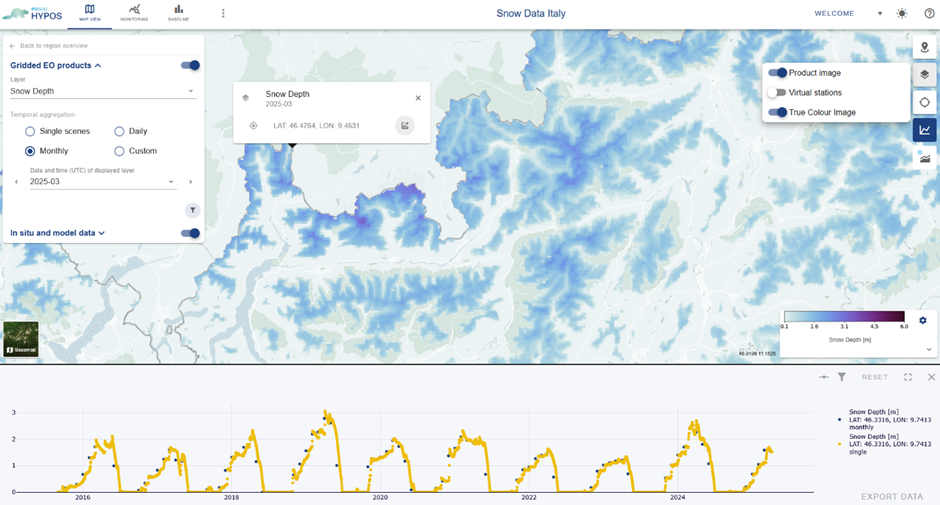

This is where space comes in. Take SnowPower, a recent EOMAP-led ESA project which has been running since winter 2024 which delivers data on snow using novel remote sensing techniques to provide information on snow depth and snow water equivalent using Europe’s Sentinel-1 SAR satellites. This data allows users to know how much water is stored as snow in the catchment area, at a much lower cost than sending an engineer with a sensor round to check it.

Whilst just a pilot, this project is set to save each site tens of millions of pounds per year, without even mentioning the reduced CO₂ emissions. This isn’t just a pretty demonstration, it is money saved right on the balance sheet.

Storage and Distribution: Methane Leak Detection and Pipeline Monitoring

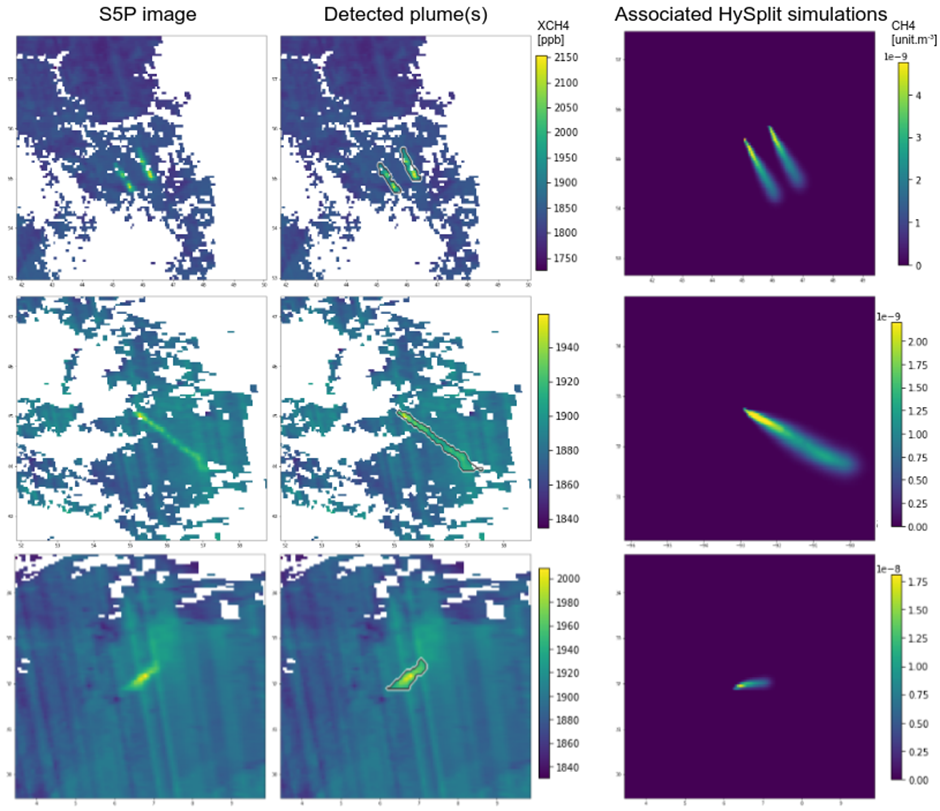

Another key point to mention is methane, a short-lived gas that traps 84x more heat than carbon dioxide over a 20-year period and has resulted in 30% of today’s global warming. This gets worse when you consider that the International Energy Agency estimates that the production and use of fossil fuels results in close to 120 million tonnes of methane emissions in 2023, with 5Mt of methane from major fossil fuel leaks around the world. However, from a business perspective, this is not just about global warming—every single gram of methane emitted is a gram of methane not sold for profit, and the leaks cause untold financial penalties in the form of fines.

Enter Methane Watch, an ESA-funded project by Kayrros SAS, which detects large-scale methane emissions using the Sentinel, Landsat, and other satellites. Satellites are especially important in this area as methane is very technically challenging to measure as it leaks across the whole energy supply chain over time. Without frequent, cross-border sensing, these emissions are basically unseen and impossible to fix.

This gets even worse for the operators once we consider regulations. Organisations such as the EU are launching new strategies that mandate leak detection with fines for non-compliance. In the face of this, satellite imagery is perhaps the most important tool to enforce these regulations, with new and improved satellites launching every year to improve monitoring capabilities.

Operation and Maintenance: Vegetation Encroachment

The next stage in the energy lifecycle is operation and maintenance. This could be a puzzling part of the chain to include, as obviously satellites cannot operate powerplants. Yet, you just need to think wider, about all operational costs.

Take the US for example. There are millions of trees right next to the National Grid’s electricity assets. The grid spends hundreds of millions of dollars per year on maintaining and mitigating risks to the infrastructure because of this. As the climate changes, storms are more frequent, and this represents a risk to your electricity supply as just one tree could cut it off. Traditionally, as per the other applications, this was investigated by sending out staff, drones, or helicopters, all of which work on a small scale but cannot scale without compounding costs.

To solve this, companies such as AiDASH use satellite data to allow organisations to manage tree growth near transmission and distribution lines. When this is combined with new techniques related to AI, tree management systems are able to predict growth many years in advance, allowing for trims, removals and herbicides to be deployed to save the power grid.

In a Massachusetts pilot, AiDASH allowed the National Grid to optimise the scheduling of vegetation pruning from 5 years to 6 years, as well as highlighting hotspots of risk for tree falling. You might think that a mere 1-year increase in the time between pruning is not a lot, but in reality, that is a saving of 17% in terms of cost and manhours.

End of Life: Decommissioning Offshore Oil and Gas Platforms

The final stage of the energy lifecycle is decommissioning: retiring oil platforms, offshore wind farms, nuclear plants, or coal assets. On the surface, it sounds straightforward: lock up and throw away the key. But in reality, it’s one of the most complex, expensive, and risk-laden stages. Decommissioning the 500+ offshore oil and gas platforms in the North Sea alone is expected to cost over €50 billion by 2040.

This is where space systems play a role. Satellites and GNSS underpin remote robotics, uncrewed surface vessels and subsea ROVs that can be operated from shore using satellite communications. GNSS ensures precise positioning; satcom provides real-time command and control. These tools reduce the need for large crewed vessels, cutting costs massively.

At the same time, Earth observation and InSAR monitor the environmental impact of dismantling, from seabed disturbance to land subsidence around retired coal or nuclear sites. And in the case of carbon capture and storage, satellites help detect leaks from wells repurposed for CO₂ storage, ensuring long-term safety and regulatory compliance.

So, while decommissioning looks like an end, it’s actually a high-stakes operational challenge where space data and services directly improve safety, cut costs, and reduce emissions.

Space for energy, in short, is about applying the data and connectivity already available in orbit to the specific challenges energy operators face on the ground. It is less about creating new constellations than about using what exists more intelligently.

Challenges and Industry Dynamics

The appeal of space for energy is obvious: measurable savings, reduced emissions, and improved resilience. Yet adoption across the sector has been slow, patchy, and uneven. The reasons lie not in the technology, but in the unique dynamics of the energy industry itself.

The first barrier is conservatism. Energy operators are among the most risk-averse organisations in the world. Grid operators are tasked with ensuring that electricity flows every second of every day; failure is not an option. Introducing new technology into this environment requires not only technical proof, but long cycles of validation, certification, and regulatory acceptance. For comparison, utilities typically evaluate grid upgrades on investment horizons of 20 to 40 years, far longer than the five-to-ten-year commercial timelines of most satellite service providers. That mismatch slows adoption to a crawl.

A second challenge is procurement complexity. Utilities are often semi-state bodies or regulated monopolies, with procurement processes designed to minimise perceived risk rather than maximise innovation. Tenders for vegetation management, for example, may be structured around helicopter patrol hours rather than outcomes like outages avoided. Even when satellite solutions are technically superior, they can struggle to fit into existing procurement frameworks. In Europe, some tenders run on cycles of three to five years, with renewal terms that lock incumbents in place and leave little room for new entrants.

A third factor is legacy IT integration. Utilities have invested billions in existing systems, grid management software, and asset databases over decades. These platforms are often proprietary, poorly documented, and resistant to integration. A satellite service that delivers imagery or alerts is of little value unless it can plug seamlessly into these existing workflows. Building that middleware layer is usually more expensive and time-consuming than acquiring the satellite data itself.

The energy sector is also shaped by regulatory pressure. Carbon pricing in the EU Emissions Trading System reached more than €90 per tonne of CO₂ in 2023. Methane rules will impose mandatory leak detection across the gas sector, with fines expected in the millions. Reliability standards for electricity grids are tightening as renewables increase volatility. Each of these pressures creates opportunities for space-enabled monitoring, but also raises the bar for evidence. A utility cannot adopt a tool because it looks promising; it must demonstrate to regulators that the system is reliable, auditable, and defensible.

Finally, there is the issue of scale. Energy infrastructure is vast: ten million kilometres of European distribution grid, hundreds of offshore platforms, and pipelines stretching across continents. Satellite services excel at providing wide-area coverage, but turning that coverage into actionable, operator-specific insights requires localisation, customisation, and sustained engagement. The industry rewards vendors that can scale not just technically but organisationally, those able to meet service-level agreements, withstand liability, and survive procurement audits. Many space start-ups underestimate these demands and fail to transition from pilot projects to full contracts.

Together, these dynamics explain why space applications in energy have not yet scaled to their full potential. The value is clear, the technology is proven, but the business model has to adapt to an industry that moves slowly, regulates heavily, and punishes failure severely.

Conclusion: Adoption Is the Real Bottleneck

The case for space in energy is compelling. Satellites are already cutting inspection costs for power lines, detecting invisible methane leaks, optimising hydropower forecasts, and enabling safer, cleaner decommissioning offshore. These are not speculative benefits. They are measurable outcomes with direct financial, environmental, and social impact.

And yet, despite these successes, adoption remains slow. The challenge is not whether satellites can deliver value; they can, and the numbers prove it. The challenge is whether utilities, regulators, and governments can adapt their systems, incentives, and procurement frameworks to integrate these tools at scale. Until that happens, many of the most promising services will remain stuck in demonstration mode, pilots praised in press releases but never embedded into core operations.

For Europe, where energy security, climate targets, and industrial competitiveness converge, this matters deeply. Every outage avoided, every tonne of methane prevented, every unnecessary vessel trip cut from offshore operations is a direct contribution to resilience and decarbonisation. Satellites are already capable of delivering these gains. What is missing is the willingness of the energy sector to buy, integrate, and trust them.

The lesson is simple but uncomfortable. The bottleneck in space is no longer rockets or satellites. It is adoption. Unless the energy industry moves faster to take advantage of the capabilities already overhead, billions in potential savings and emissions reductions will remain on the table. And in a decade defined by energy transition and climate urgency, that delay is a luxury Europe cannot afford.