The satellite communications (SATCOM) market in 2024 is a landscape defined by a handful of dominant players, each of whom is steering the direction of the industry. While new entrants continue to make their mark, it is clear that SpaceX, Viasat, Inmarsat, SES Satellites, EchoStar Corporation, and Eutelsat OneWeb remain firmly in control, shaping the market for years to come.

But while many look at the increasing competition and growing demand for global connectivity, it’s important to ask: Is the market really changing, or are these players simply consolidating their hold on a rapidly expanding industry?

In this analysis, we’ll take a look at the major players, their market shares, and the wider implications for the SATCOM sector as a whole. But first, let’s break down the numbers that dominate the 2024 landscape.

This article is an extract from a larger report being released by NebuLink within the next two months. Highlights of trends are included in this article, but the full workings is reserved for the report. If you are looking for SATCOM market sizing before then, get in touch: alistair@nebulink.co.uk.

The Market Share Breakdown: Who’s Leading in 2024?

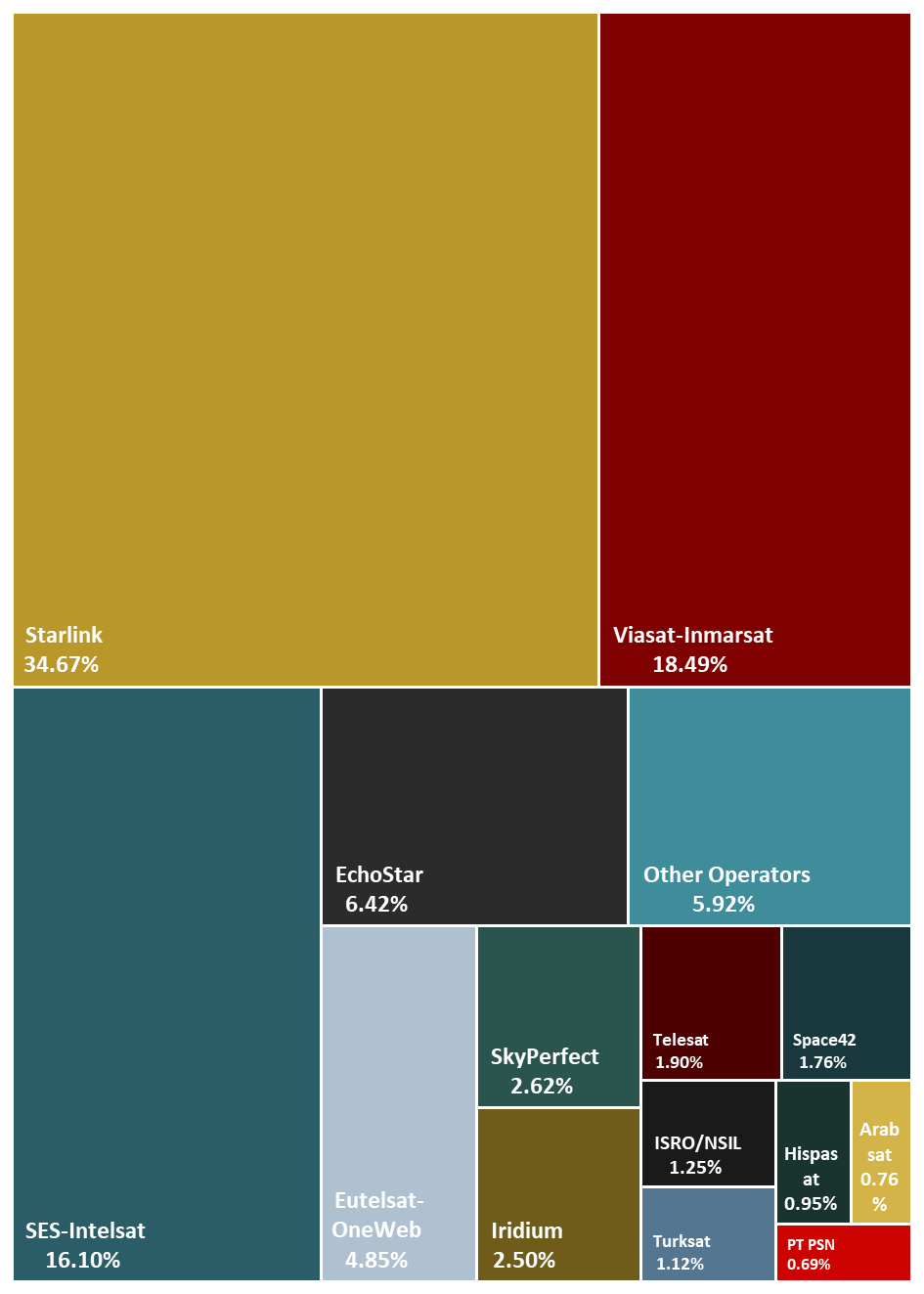

It’s no surprise that the SATCOM market in 2024 is largely shaped by just a handful of operators. The market share distribution is glaringly clear:

Starlink: 34.67% As the undisputed leader in low-Earth orbit (LEO) satellite services, Starlink has firmly cemented its place at the top. Its rapid expansion into underserved regions, coupled with its ability to deliver low-latency, high-speed broadband, means it continues to expand its influence. Starlink’s role in bridging the digital divide cannot be overstated—if anything, its impact is only growing as its constellation of satellites expands.

Viasat-Inmarsat: 18.49% The merger between Viasat and Inmarsat has positioned this combined entity as a significant player in mobility solutions. With expertise across sectors like aviation, maritime, and defence, the merger provides a robust foundation for delivering high-speed broadband services across industries that require global mobility and reliable connectivity.

SES-Intelsat: 16.10% The SES-Intelsat alliance continues to dominate in geostationary orbit (GEO) satellite communications. This partnership remains crucial for supporting telecom operators, media broadcasters, and government services, offering stable, long-term communication solutions that are essential for daily operations across numerous sectors.

EchoStar: 6.42% A familiar name in satellite broadband and mobile services, EchoStar continues to hold a solid position in the market. With a focus on remote and underserved areas, EchoStar’s global expansion is helping to close the connectivity gap.

Other Operators: 24.84% There remains a significant portion of the market that is shared by other operators, including Eutelsat-OneWeb, Iridium, SkyPerfect, Telesat, and others. Each of these companies continues to innovate and make strides in specialised services like satellite broadband, mobile satellite services, and IoT connectivity.

What This Market Share Means for the Industry

At first glance, the dominance of a few key players might seem like a sign of stagnation or lack of competition. However, the reality is more nuanced. These market leaders are not just holding their ground—they are continuing to evolve, setting the pace for the next phase of SATCOM innovation.

-

LEO Satellites Are Leading the Charge The rise of LEO satellite networks is not just a trend; it’s a fundamental shift in the way global connectivity is provided. Starlink, as the largest player in this space, is leading the charge. With its vast constellation and continuous upgrades, it remains at the forefront of delivering high-speed, low-latency broadband to areas that terrestrial networks simply cannot reach. Its rapid rollout of satellites is setting new expectations for connectivity.

-

Mergers Are Driving Consolidation, Not Competition The Viasat-Inmarsat merger is a clear example of industry consolidation. While some might see this as an attempt to create a European alternative to SpaceX’s Starlink, this merger isn’t purely about creating a competitor; it’s about efficiency and increasing scale. It’s about bringing together capabilities that are already being shared across major projects like IRIS² and Galileo. Only time will tell if this consolidation is enough to compete, or whether these operators will continue to have their market share taken by Starlink.

-

GEO Satellites Still Play a Crucial Role Despite the rise of LEO, GEO satellites from SES-Intelsat remain a cornerstone of the SATCOM industry. These satellites continue to offer stable, reliable services across industries like telecom, media, and government, and will continue to be indispensable for a range of applications from broadcasting to secure communications.

-

Room for Specialised Operators While the larger players dominate, the other operators like Iridium, SkyPerfect, and Telesat continue to find niches in specialised satellite communications, particularly in IoT, remote connectivity, and government contracts. Their ability to offer tailored solutions is likely to continue to sustain their relevance in the market.

Looking Forward: What Comes Next for SATCOM?

The industry’s future is not solely dictated by the market share of these few dominant players. While the LEO and GEO network arguments will remain central to global connectivity, the next big wave in SATCOM will be driven by the following:

Cross-Sector Collaborations: Expect to see more integrated solutions that bridge the gap between satellite and terrestrial networks, particularly in areas such as 5G integration and cloud-based satellite services.

Technological Innovation: Software-defined networking, cloud-based satellite networks, and AI-powered management systems will transform how SATCOM services are delivered, offering greater scalability and network efficiency.

Increasing Demand for Global Mobility: As the world becomes more interconnected, the need for high-speed, reliable mobile satellite services will continue to grow. Viasat-Inmarsat and Starlink are likely to benefit the most from this shift, as more industries, aviation, maritime, and defence, seek seamless global mobility solutions.

The SATCOM market is anything but stagnant, even if the same key players continue to dominate. These players are evolving, and the next phase of growth will likely see an even greater convergence of GEO, MEO, and LEO services to meet the growing demand for global connectivity.

Want to learn more?

This is a preview of an upcoming SATCOM market report where we explore these dynamics in detail, covering everything from technological advancements to the competitive landscape, as well as future growth predictions.

Reach out to discuss how this analysis can impact your strategy or book a call with me at alistair@nebulink.co.uk